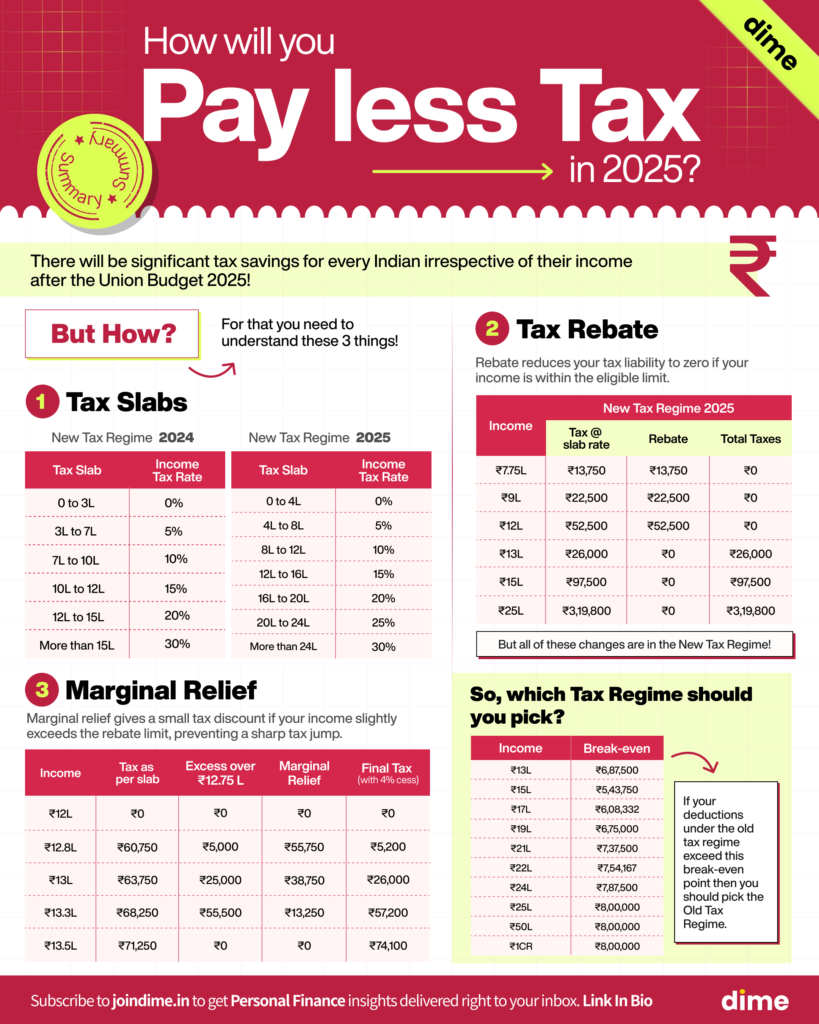

Income up to 12,75,000 is tax free! —That’s the headline of the budget 2025. But, what’s behind this? And is that the only positive outcome for you? Well, not exactly. So let’s see what are the exact changes with income tax and how it is going to benefit you!

Income Tax Slab Changes

New Tax Regime 2024

New Tax Regime 2025

The slabs have changed completely and a new rate of 25% applicable between 20,00,000 to 24,00,000 has also been introduced.

The best part? Now you don’t pay 30% straight over 15 Lakhs, rather on above 24 Lakhs.

How is it going to affect you?

Here’s how much you would save under different income levels, thanks to the updated rules:

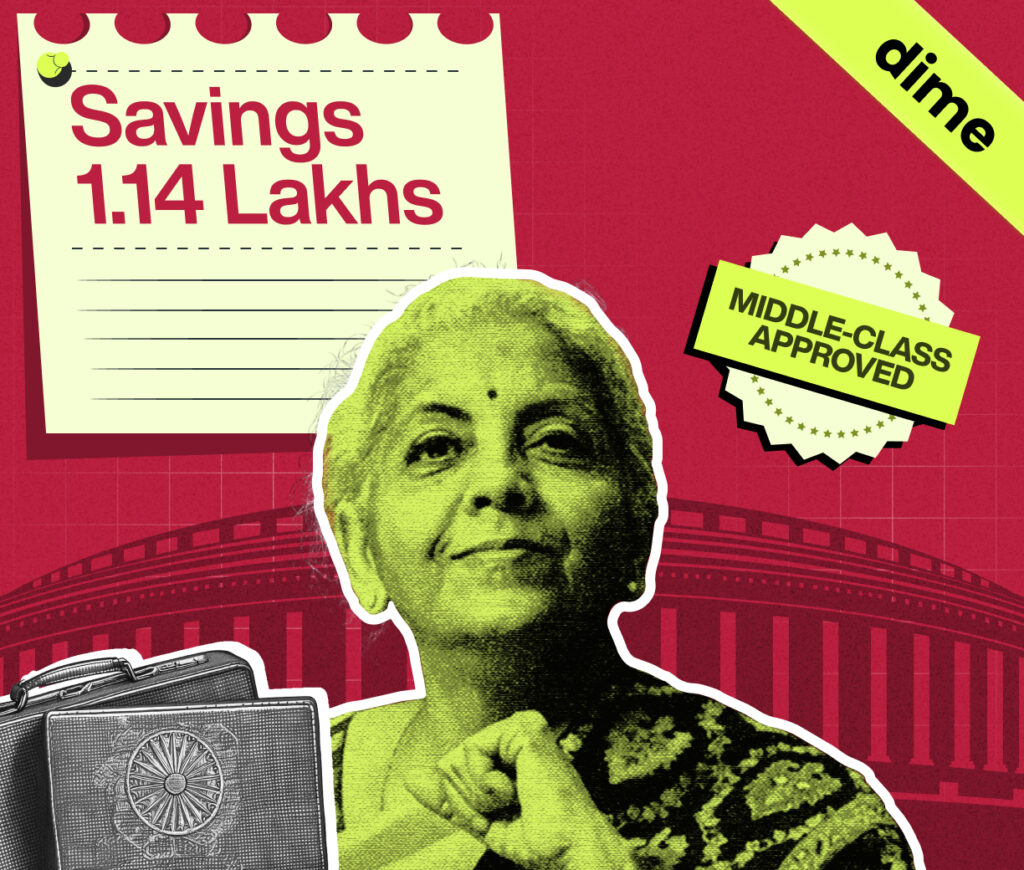

As you can see the maximum savings caps at 1,14,000 and though your income might rise but after 25L of income you are going to save any additional amount.

But, this saving is not just because of change in the slab rates if you notice. Then what?

How does Rebate help?

Assume you need to pay Rs10 as Tax to the Government , but the Govt. says I am running a discount offer and will give you a 100% discount on your Tax. Well, that is called a Rebate which the Government gives up to a certain income limit.

Here’s how the Rebate rule has changed:

So let’s have a look how these updated Rebate rules help you save tax:

As you can see the help from Rebate stops at 12.75 Lakhs, but you are still saving tax on each income level. How does that happen? For that you’ll have to understand—

How Marginal Relief helps?

While rebate is only given till a specific threshold, marginal relief kicks in just beyond it—offering a small break instead of a full discount!

Here’s how it helps:

However, these benefits also stop at ₹13,50,000 and after this the savings are only because of the Improvised Tax slabs and rates.

But here’s the catch!

Even if your total income is below ₹12.75L, you still pay tax on special incomes like capital gains. Let’s break it down with an example:

Saroj earns ₹9L in FY 25-26. Out of this, ₹2L is profit from stocks she bought in 2020.

Even though her total income is under ₹12.75L, she still pays tax on her capital gains.

That’s because capital gains tax applies separately—so, even if your income qualifies for a rebate, these taxes still apply!

Is the Old Tax regime dead?

The old tax regime remains unchanged for another year and it seems that the Old tax regime is going to be phased out though not officially. Here’s why:

Simpler Compliance:

No need for complex tax planning, and claiming exemptions or deductions under the new system.

Higher Tax-Free Limit:

The new regime exempts income up to ₹12.75L, while the old regime taxes above ₹5.5L.

Lower Tax Liability:

The Tax Payable is mostly lower under the New Tax Regime unless you have a ton of deductions under the Old Tax Regime!

72% already use the new tax regime, and recent benefits will definitely push this number higher!

Which one should you pick?

Refer this table to understand for what amount of deductions under different income levels, which regime makes sense:

So, now you know which Tax Regime to pick, right?

Is that it?

Nope, here are a few more updates on you Tax money:

1. TDS (Tax Deducted at Source)

TDS is a tax deducted from your income (salary, interest, rent) before payment, ensuring tax is collected upfront.

2. TCS (Tax Credited at Source)

TCS (Tax Collected at Source) is a tax the seller collects from the buyer and pays to the government.

Voila! That’s it! Here’s how every Indian will be saving on taxes after the Union Budget 2025, that too without spending on tax saving assets or finding out hidden methods.

Summary

Refer the image below for the summary of the entire Read. Hope you enjoyed the Read!