Learn how you can save more through smart use of tax exemptions and deductions. This guide will help you save more and pay less tax.

Taxes are something everyone has to deal with, and understanding how they work can make a big difference in how much you actually pay. By using tax exemptions and deductions wisely, you can significantly reduce your taxable income.

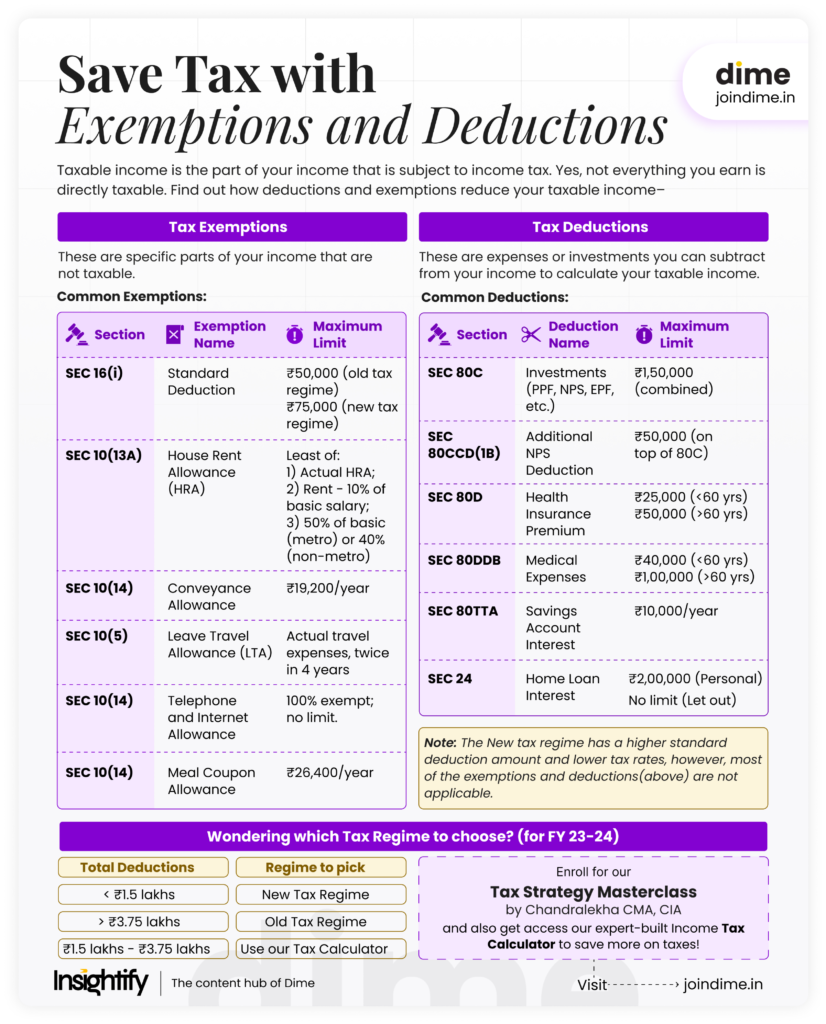

But first, what are these terms?

Taxable Income:

This is the portion of your income that is subject to income tax. Yes, not everything you earn is directly taxable.

Tax Exemptions:

Tax exemptions are specific parts of your income that are not taxable. Certain allowances or parts of your salary are exempt (subtracted) from being taxed, reducing your total taxable income.

Here are a few common Tax exemptions:

| Section | Exemption Name | Applicability | Maximum Limit |

| SEC 16 (i) | Standard Deduction | Flat deduction for salaried employees (This is default, no action required by employee) | ₹50,000 (under old tax regime) ₹75,000 (under new tax regime) |

| SEC (13A) | House Rent Allowance (HRA) | For employees paying rent and receiving HRA | Least of: 1) Actual HRA; 2) Rent – 10% of basic salary; 3) 50% of basic (metro) or 40% (non-metro) |

| SEC 10 (14) | Conveyance Allowance | For commuting between home and office | ₹1,600/ month or ₹19,200/year |

| SEC 10 (5) | Leave Travel Allowance (LTA) | Travel within India for self and family | Actual travel expenses, twice in block of 4 years (e.g.2022-2025) |

| SEC 10(14) | Meal Coupon Allowance | Food allowance provided by your employer for meals on working days. | ₹ 26,400/year |

| SEC 10 (14) | Telephone and Internet Allowance | Reimbursements for telephone and internet expenses for official purposes. | 100% exemption on actual bills for business use; no prescribed limit. |

Tax Deductions:

These are expenses or investments you can subtract from your income. These are not part of your salary. You get them by investing, saving, or spending on specified avenues. So basically you need to spend money (expense/invest) to claim them.

Here are a few common exemptions:

| Section | Deduction Name | Meaning/Applicability | Maximum Limit |

| SEC 80C | Investments (PPF, NPS, EPF, etc.) | Contributions to PPF, NPS, PPF, ELSS, etc | ₹1,50,000 (combined limit). |

| SEC 80CCD(1B) | Additional NPS Deduction | Extra deduction for NPS contributions | ₹50,000 (above the ₹1.5 lakh limit under Section 80C). |

| SEC 80D | Health Insurance Premium | Medical insurance for self, spouse, kids, and parents (dependents) | ₹25,000 (<60 years), ₹50,000 (>60 years) for parents. |

| SEC 24 | Home Loan Interest | Interest paid on Home Loan | ₹2,00,000 (self-occupied property); No limit (Let out property) |

| SEC 80TTA | Savings Account Interest | Interest from savings accounts | ₹10,000/year. |

Still Confused? Let’s understand with the help of an example:

Here’s annual income and deductible expenses of Rajesh, a product manager, living in Mumbai:

| Income (Annual) | Amount (₹) | Expenses/Investments (Annual) | Amount (₹) |

| Basic Salary | ₹14,40,000 | Contribution to NPS | ₹60,000 |

| House Rent Allowance | ₹1,44,000 | Contribution to EPF | ₹1,72,800 |

| Conveyance Allowance | ₹60,000 | Health Insurance Premium (personal, spouse < 60 years, 1 kid) | ₹24,000 |

| Leave Travel Allowance | ₹30,000 | Health Insurance Premium (parents > 60 years) | ₹48,000 |

| Meal Coupons | ₹26,400 | Rent paid (annual) | ₹2,40,000 |

| Interest on Savings Account | ₹11,000 | Home loan interest paid | ₹1,20,000 |

| Telephone and Internet Allowance | ₹6,000 | Rent paid (annual) | ₹2,40,000 |

| Total Income | ₹17,17,400 | Total Expenses/Investments | ₹6,64,800 |

Total Deductions + Exemptions:

| Deduction/Exemption | Amount (₹) [Old-Tax Regime] | Amount (₹) [New-Tax Regime] |

| Standard Deduction [Section 16] | ₹50,000 | ₹75,000 |

| HRA Exemption [Section 10(13A)] | ₹96,000 | Not applicable |

| LTA Exemption [Section 10(5)] | ₹30,000 | Not applicable |

| Conveyance Allowance [Section 10(14)] | ₹19,200 | ₹19,200 |

| Telephone/Internet Allowance [Section 10(14)] | ₹6,000 | Not Applicable |

| Meal Coupon Allowance [Section 10(14)] | ₹26,400 | Not Applicable |

| EPF [Section 80C] | ₹1,50,000 | Not Applicable |

| NPS [Section 80CCD] | ₹50,000 | Not Applicable |

| Health Insurance [Section 80D] | ₹72,000 | Not Applicable |

| Home Loan Interest [Section 24] | ₹1,20,000 | Not Applicable |

| Savings Interest [Section 80TTA] | ₹10,000 | Not Applicable |

| Total Deductions/Exemptions | ₹6,29,600 | ₹94,200 |

Taxable Income Calculation:

| Category | Amount (₹) [Old-Tax Regime] | Amount (₹) [New-Tax Regime] |

| Total Income | ₹17,17,400 | ₹17,17,400 |

| Total Deductions/Exemptions | ₹6,29,600 | ₹94,200 |

| Taxable Income | ₹10,87,800 | ₹16,23,200 |

| Tax Liability | ₹1,44,394 | ₹1,84,038 |

Note: New tax regime has a higher standard deduction amount and lower tax rates, but most of the exemptions and deductions are not applicable.

Wondering which Tax Regime to choose?

The choice between the old and new regime largely depends on your income level and the amount of deductions and exemptions you can claim.

Here are a few calculations that can help you decide between the old vs the new tax regime:

| Total Deductions | Which Regime is Beneficial? |

| ₹1.5 lakhs or less | New Tax Regime |

| More than ₹3.75 lakhs | Old Tax Regime |

| Between ₹1.5 lakhs and ₹3.75 lakhs | Depends on Income Level |

One simple question before we part,

What if you could keep more of your salary?

Our Tax Strategy Masterclass helps you do exactly that! We help you learn the proven hacks that let you restructure your salary, choose the best tax regime, and legally save big on taxes.

Oh, did we mention? Inside our Masterclass, you also get our flagship and most famous Old vs New tax Regime Tax Calculator.

Access to our powerful, expert-built Income Tax Calculator to help you make smart decisions and save big on taxes.

Here’s a sneak peak into it

Enroll for our Tax Strategy Masterclass today to save more on taxes!

SUMMARY

Refer the image below for the summary of the entire Read. Hope you became smarter with money now.