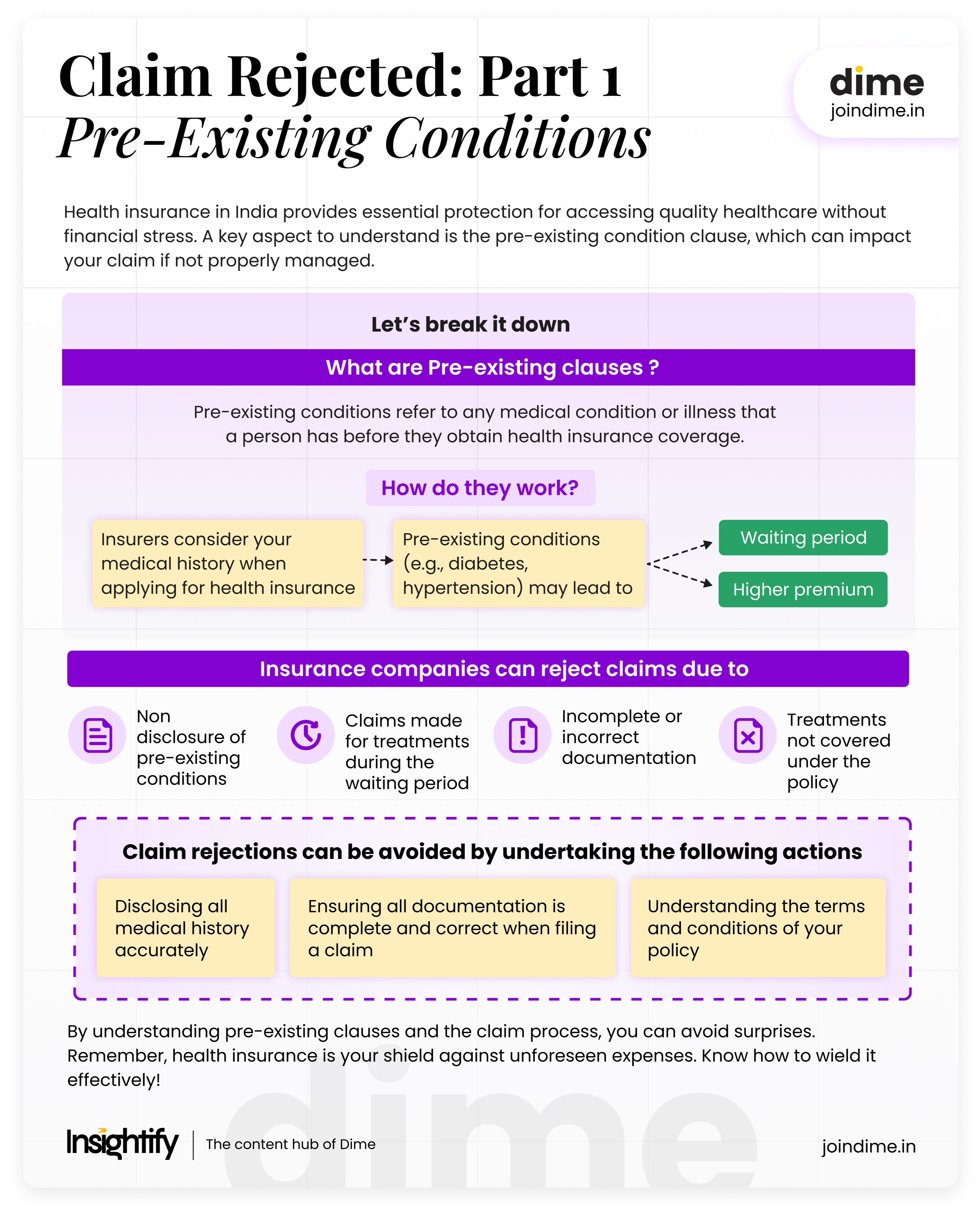

Health insurance in India is more than just a policy—it’s a safety net that ensures you and your family can access quality healthcare without financial stress. Understanding how it works, particularly the pre-existing condition clause, is crucial, as this clause can lead to claim rejections when coverage is needed most. Let’s explore how this clause impacts your policy with real-life examples.

How Does Claim Rejection Work?

In a notable case reported by the Economic Times, a widow successfully secured Rs 28 lakhs in damages after her husband’s health insurance claim was initially denied. The insurance company had rejected the claim, citing a pre-existing condition as the reason. However, the court ruled in the widow’s favor, stating that the death was not caused by any concealed or undisclosed pre-existing condition at the time the policy was issued. As a result, the insurance company could not legally deny the claim.

This case highlights the common reasons why insurance claims might be rejected and how they happen:

- Non-disclosure of Pre-existing Conditions: If the insured person fails to disclose any pre-existing medical conditions at the time of purchasing the policy, the insurance company might reject the claim if the condition directly contributes to the health issue for which the claim is made.

- Claims During the Waiting Period: Many policies have a waiting period during which certain treatments or conditions are not covered. If a claim is made for treatment within this period, the insurer can deny it.

- Incomplete or Incorrect Documentation: Submitting incomplete or incorrect paperwork can lead to claim rejection. It’s crucial to provide all required documents accurately.

- Treatments Not Covered Under the Policy: If the treatment or condition for which the claim is made is not covered under the policy terms, the insurance company is within its rights to reject the claim.

What Are Pre-Existing Clauses?

Pre-existing conditions refer to any medical condition or illness that a person has before they obtain health insurance coverage. These conditions are often documented by medical records, and insurers usually impose specific clauses related to them.

How Do They Work?

When you apply for health insurance, insurers usually ask for your medical history. If you have a pre-existing condition like diabetes, hypertension, or a heart condition, the insurer may either:

Impose a waiting period during which they will not cover expenses related to the pre-existing condition

Increase the premium to offset the risk

Exclude coverage for the pre-existing condition altogether

Imagine Mr. Sharma, who has diabetes, applies for health insurance. His policy might have a waiting period of 2-4 years for diabetes related treatments. This means if he incurs medical expenses due to diabetes within this period, the insurance will not cover it.

However, claim rejections can be avoided by undertaking the following actions:

- Disclosing all medical history accurately when applying for insurance

- Understanding the terms and conditions of your policy, especially exclusions and waiting periods

- Ensuring all documentation is complete and correct when filing a claim

According to Policy Bazaar, out of the total claims rejected, 75% rejections are caused due to limited understanding of health policy and undisclosed pre-existing diseases. This highlights the need to have a better understanding of health policies to avoid claim rejections.

Let’s understand this with an example:

Imagine Mrs. Singh, a 45 year old woman with a history of hypertension. She buys a health insurance policy.

Here’s how her experience might unfold:

| Component | Details |

| Pre-Existing Clause | Her policy includes a 3-year waiting period for hypertension related treatments. During this time, if she incurs any medical expenses due to hypertension, her insurance will not cover them. |

| Claim Submission | Two years into her policy, Mrs. Singh submits a claim for hospitalization due to a sudden heart issue. She provides all necessary documents, including hospital bills and doctor’s notes. |

| Claim Rejection | The insurance company rejects the claim, citing her pre-existing hypertension as the cause of the heart issue. They state that the claim falls within the waiting period. |

| Resolution | Mrs. Singh reviews her policy and discovers that the heart issue is not directly linked to her hypertension. She submits an appeal with additional medical evidence. The insurer re-evaluates and approves the claim, covering her expenses. |

This scenario demonstrates how understanding your policy and ensuring accurate documentation can influence claim outcomes.

Health insurance is essential for financial protection against medical emergencies. Understanding pre-existing clauses and the claim process can prevent unpleasant surprises. By disclosing medical history accurately, keeping thorough records, and understanding policy terms, you can navigate the health insurance landscape with confidence.

Remember, health insurance is not just a piece of paper, it is your shield against unforeseen medical expenses. Make sure you know how to wield it effectively!

Summary

Refer the image below for the summary of the entire Read. Hope you became smarter with money now.

FAQs

Are treatments for pre-existing conditions automatically covered after the waiting period?

Once the waiting period ends, treatments for disclosed pre-existing conditions are generally covered according to your policy’s terms. However, coverage may have limits on specific treatments, so review these details with your insurer. Always keep documentation of the waiting period completion to avoid complications when filing claims.

Is it necessary to disclose all medical history when buying health insurance?

Yes, it is essential to disclose your complete medical history when purchasing health insurance. Providing accurate details on conditions like hypertension, diabetes, or surgeries helps avoid claim rejection due to “non-disclosure.” This transparency ensures a smoother claims process and prevents issues from arising if a related medical condition surfaces later.

Can a claim for a health issue unrelated to a pre-existing condition be rejected?

Generally, insurers should not reject claims unrelated to a pre-existing condition. However, if the insurer believes the pre-existing condition contributed to the health issue, they may reject the claim during the waiting period. Providing clear documentation that differentiates the conditions can help in case of an appeal.

Can my premium be increased because of a pre-existing condition?

Yes, insurers may increase your premium if you have a pre-existing condition. Higher premiums compensate for the additional risk associated with covering chronic conditions like diabetes or heart disease. Some insurers offer plans with fixed premiums but exclude certain conditions; check policy terms to choose what works best for you.